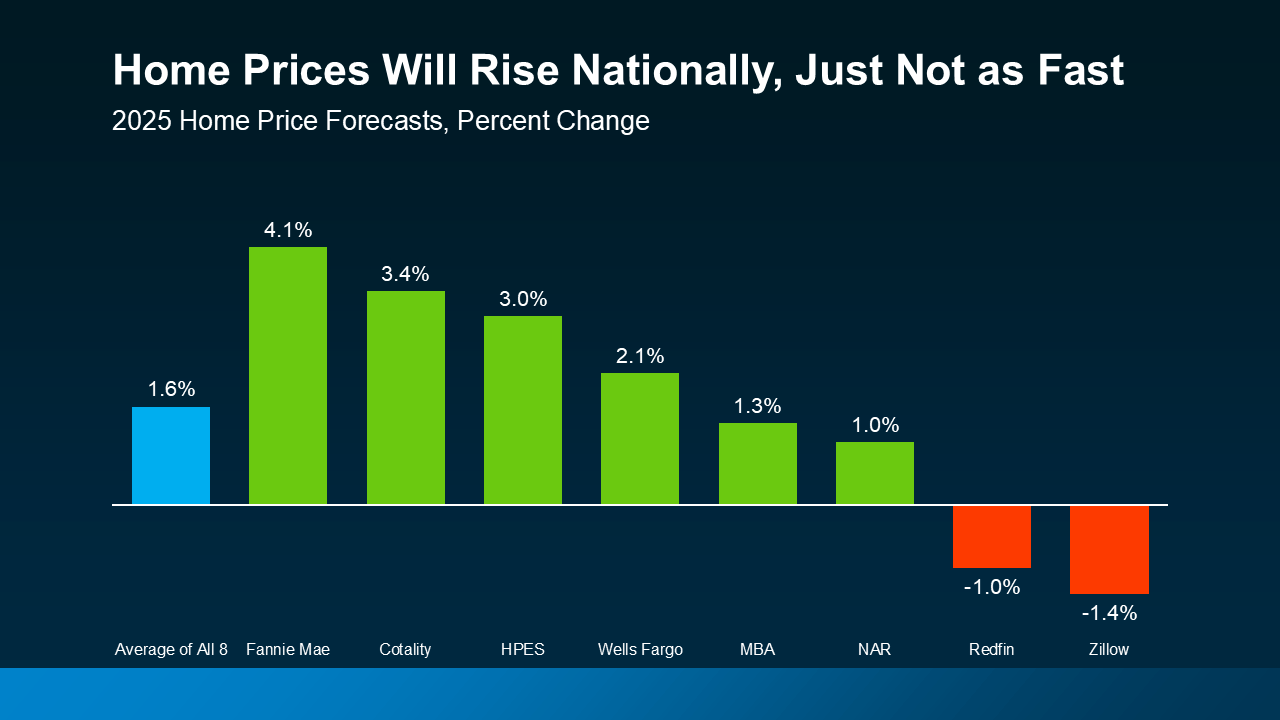

Be Ready for the Rebound

If your clients have tried to sell a home this year, but couldn’t get the price they were hoping for, they’re not alone. Today’s market can feel slow and discouraging. History tells a different story, though: the housing market always bounces back. In the ’80s, during the 2008 financial crisis, and even through 2020, sales fell—and then recovered. Some industry analysis suggest that conditions may improve as mortgage rates change over time. While slowdowns are common, history shows that housing markets often recover.